May 20, 2015

Rarely a week goes by without a prominent columnist or think tank warning of an impending provincial credit crisis.

As the Mowat Centre pointed out in a recent report, these doomsday forecasts are overblown. And yet as The Globe and Mail’s debt series has noted, it’s hard to deny that the provinces, whose gross debts collectively equal roughly 50 per cent of GDP, have a debt problem.

There are some who believe the provinces aren’t the only subnational governments that ought to borrow less. Municipal governments — whose capital-market activities go largely unnoticed — are also accumulating significant debts. Net municipal borrowing has been positive every year since 2000, and by 2012 gross municipal liabilities were approaching 10 per cent of Canadian GDP. Some prominent politicians and economists are alarmed.

Should they be? Money spent on interest and principal payments is, after all, money otherwise available for local services. It is also money that future residents have to repay.

But municipalities are not borrowing to cover day-to-day operations. They are borrowing (by virtue of provincial law) to finance roads, bridges and other infrastructure and capital assets. This is good news: These assets are the foundations of urban prosperity, and Canada’s urban infrastructure is in dire need of expansion and repair.

Continue reading

Of course, municipalities can pay for infrastructure in other ways. They can raise taxes or user fees or, as Ottawa Mayor Jim Watson has suggested, ask for more from the federal government (which borrows at lower interest rates). But the political appetite for tax hikes is low, and senior levels of government face their own fiscal challenges. For practical reasons, borrowing must be part of the solution.

Fortunately, it also makes good sense. Borrowing is an equitable and efficient means of financing long-term capital assets. It ensures that infrastructure costs are not paid solely by today’s taxpayer, but by the debt charges of future users as well.

Granted, borrowing carries risk. Governments have to ensure they have adequate revenues (including own-source revenues and transfers) to meet debt payments. They also have to protect their finances from spikes in interest rates.

But Canada’s municipal borrowers are not nearly as sensitive to interest-rate shocks as Canadian provinces.

Municipal debts are a fraction of provincial liabilities, and provincial rules prohibit municipalities from borrowing to excess. Municipalities also issue fixed-interest-rate debt and assume virtually zero refinancing risk — the principal on municipal bonds is typically amortized or repaid by sinking-fund revenues. Finally, municipalities have the capacity to reduce borrowing in a way that the provinces, which borrow to finance capital and operating deficits, do not. So a sharp increase in borrowing costs would not trigger a municipal debt crisis.

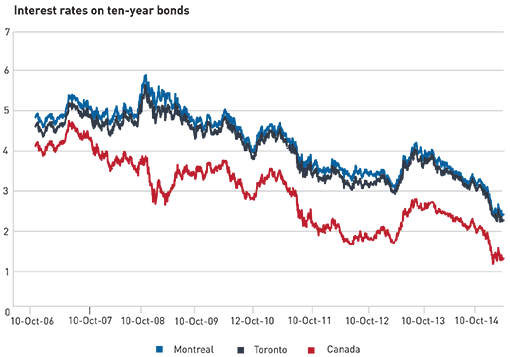

It would, however, undermine capital investment, which is yet another reason why infrastructure-starved cities ought to borrow now, while interest rates are low and demand for long-term bonds is strong. As of April 8, Toronto could lock in 10-year debt at an annual interest rate of 2.27 per cent. Montreal — generally considered among the least creditworthy of Canada’s major cities — could lock in at 2.42 per cent (see figure below).

Not all municipalities should borrow more. And not all borrowing is productive. But the recent spike in municipal borrowing is not, in and of itself, cause for alarm. To the contrary, it suggests cities are finally getting serious about addressing their infrastructure deficits.

Fiscal hawks should worry less about overall debt levels and more about the decisions of particular governments: whether they are borrowing too much or too little and for the right projects.

Source: BMO Capital Markets, author’s calculations.

—

Kyle Hanniman is a policy associate at the Mowat Centre the author of Mowat’s recent report, Calm counsel: Fiscal federalism and provincial credit risk.

Release Date

May 17, 2015

Publication

The Globe and Mail

Author

Kyle Hanniman